Simba, the upcoming African Fintech company has launched a new card to ease money transfer services for African immigrants in the USA. With transfer of funds free for a Simba-to-Simba card, the African Fintech has taken another giant step in its mission of providing the African immigrant communities with access to financial products and services that make it easier to save, support loved ones, and thrive.

Founded by Simon Tiemtore, a West African Immigrant from Burkina Faso, Simba is positioned to provide a strong response to the multi-faceted challenges facing African immigrants when it comes to financial transactions. From money transfer amongst the immigrants to remittances, and a broad range of other fresh opportunities, the services offered by Simba will break new grounds, says Simon Tiemtore in the following Q & A.

Could we start with why you created Simba?

When I came to the U.S., I relied on my community to learn where to bank, how to build credit, to send money home and rent an apartment. It was a confusing and difficult process. Millions of immigrants living in the U.S. or coming to the U.S. still face the same issue. Like many of us, we are committed to give back. For me, it was easier to make banking skills to the service of immigrant communities here in the U.S. This is how Simba was ‘born’. We want to make access to banking services affordable to ALL.

Can you make an introduction of the company and its key services and products?

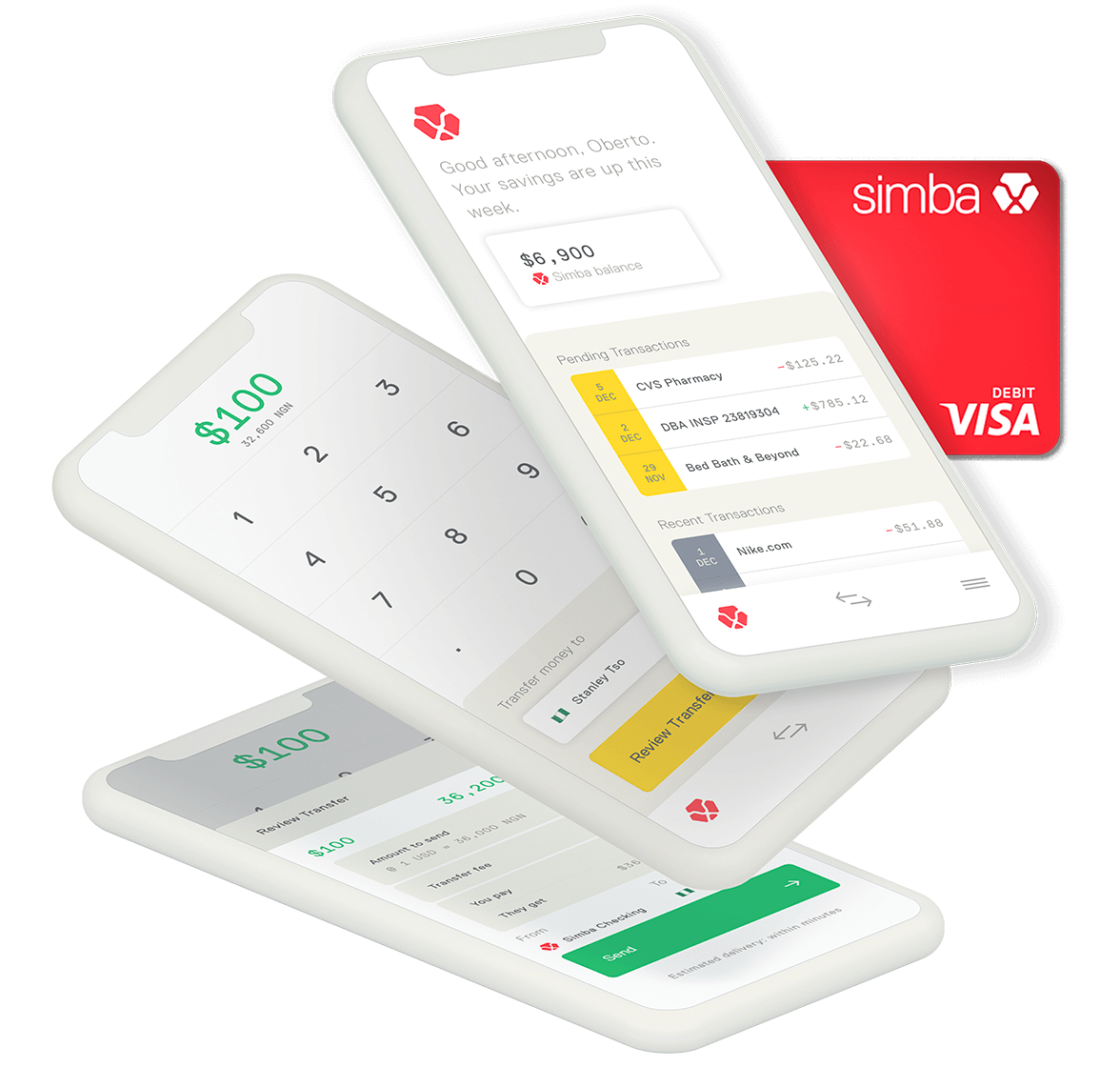

Today, Simba offers no fee mobile banking services coupled with no fee remittances in response to the needs of the African diaspora in the U.S. Simba offers the latest mobile banking services, including instant Simba-to-Simba customer transfers, contactless debit cards on the Visa network and more.

While we are ‘young’ as a company, we are planning, growing organically, introducing tailored made new products, and services in the near future. Some upcoming products include loans, rotational savings programs, wealth management and insurance over the next year.

Additionally, we’re partnering with institutions in Africa to increase remittance beneficiary services, including cash pick-up, mobile top-up and bill payment, so we are a complete solution for Africans both in the U.S. and at home. Very soon, Simba will be offering intra-Africa payments services.

Let’s talk about the Simba card that was recently launched, what is the business logic behind the card?

We coupled our services with a debit card (both physical and virtual), so that Simba customers could not only have access to their money whenever they need it, but also use their cards for online payments. We are providing ALL banking benefits in one application or account.

How easy is it to obtain the card and what safety guarantees are there for its efficacy?

Simba was built with safety and security as a top priority from day one.

Simba works under a U.S. bank license, providing complete FDIC insurance up to $250,000 USD. Additionally, Simba operates on the VISA Network, so your card is accepted anywhere VISA is accepted. Signing-up for Simba takes minutes and can be done entirely from your phone.

What does the African diaspora stand to gain from using the Simba Card and services?

Traditional U.S. Banks do not understand the immigrant journey. Their products and services are not built around the needs of immigrants, including the challenges associated with getting a bank account without a SSN, sending money home effectively and building credit to secure loans. Simba is built around the needs of the African diaspora. We’ve built a network of ambassadors and relationships with community organizations, so we are continually working within the community to learn how we can better support you. Our communities are part of our design process. Simba is built for us and by us.

There are similar services out, what is it that makes Simba unique, any particular pecks that your clientele gets by using Simba services?

We are unaware of a company today which is offering the African diaspora a complete set of products and services modeled around their needs. We are working in both the U.S. and in Africa to meet the demands of Simba clients in the U.S. and in their home countries.

On the money transfer part, how well is that working?

We first implemented a card-to-card money transfer solution built on Visa technology. This is the future – it’s instantaneous, free and you can send large dollar amounts daily.

It’s a great first solution, but we realize not all banks in African countries accept these transfers today. While the card acceptance rates are increasing quickly, we wanted to ensure our customers have other options for sending money to their loved-ones back home, so we’ve integrated other remittance providers allowing us to do other money transfer options, including: card to bank, cash pick-up and mobile top-ups. These partners will be no fee as well and rolling out starting in late November 2021.

We did see that there were still a number of key African countries missing on the list like Nigeria, Cameroon and others, what efforts are you and your team making to make sure Simba services cover all not just parts of Africa?

We are currently covering 15 countries and adding more countries. Nigeria and Cameroun will be covered by the end of November. Our brothers and sisters from Nigeria and Cameroun and any other country not currently cover can still sign up on Simba to enjoy the no fee banking and the instant no fee local transfer in the U.S. With the Simba to Simba instantaneous and free transfer, natives of those countries can still use Simba tools to transfer funds within the communities.

From your perspective how critical is the role of the diaspora in the development of Africa?

Remittances from the U.S. back to Africa are some of the largest direct investments in Africa today and are key to development. Unfortunately, it is the most expensive. This is why we believe remittances should be effortless and free; remittances are putting food on the table, family members through college, and paying basic bills. it is about time we democratize money transfer. Simba does just that.

What are some of the challenges that you have faced getting Simba operations and services running?

While I officially began this journey three years ago, I’ve wanted to build Simba for almost two decades. Like many small companies, it hasn’t always been easy, but we’re excited to launch and begin working within the community to provide a better solution.

We’ve found many companies and investors in the U.S. that are supportive of what we’re building, but unaware of the immigrant journey and the unique daily hardships they are facing. We’re helping to bridge this gap in the market.

From early indicators, may we know how the public has so far responded to the launch of the Simba card and accompanying services?

The community is excited for Simba and has been incredibly supportive. We’re eager to keep improving our products and services and to build a better experience for everyone. Investors are also very excited about the growth prospects in payment sector in Africa, so we are seeing a lot of interest in what we are doing.

The VISTA Group that you lead has been in the news with the rapid growth of its banking portfolio across Africa, can you shed some light on this for us?

The Vista Bank Group was the first step in building my vision for a complete banking solution for Africans. Coupled with Simba, we’ll offer an end-to-end offering for Africans globally. We are currently operating in Guinea, Gambia, Sierra Leone and Burkina-Faso and soon expanding our operations in 20 countries in Africa. This will enable us to better respond to our clients intra-Africa trade needs and become a key player under the African continental free trade area. Vista will also serve as a strategic partner for Simba in providing a point of services to Simba users in Africa.

What is your take on the African Continental Free Trade Agreement, what opportunities do you see in it for Simba and the Vista Group?

AfCFTA aims to create a single market for goods and services in Africa. Solving cross-border payment within the continent is critical in exponentially increase intra-Africa trade. This creates a massive opportunity for payment companies like Simba and for Vista Bank which provides the payment infrastructure to Simba. While Simba is well positioned to provide payment services, Vista Bank will provide the trade instruments to large corporates to unlock the full potential of AfCTA. Both Simba and Vista are partnering with Afreximbank and will leverage Pan-African Payment and Settlement System (PAPSS) to provide payments and trade services in the continent. So, the AfCFTA provides a unique growth opportunity for both Simba and Vista Group.

When you look at Africa what makes you hopeful and what are your fears?

Despite certain securities issues in parts of Africa, I have no fears whatsoever. We have been tested before and succeeded and will continue to thrive. To the contrary, I am super optimistic and bullish about Africa, the fastest growing region in the world. There is a reason why everyone wants to invest in Africa today.

Any last word to the large African diaspora out there on the merits of using Simba services?

Simba was built by the community for the community with the goal to empower the community financially. So, I will encourage them to sign up and take full advantage of the free banking and free transfer services that Simba offers. They worked hard to earn their money and they deserve to enjoy it fully without paying unnecessary fees for outdated services. They must be confident that Simba is here to empower them for our success is tied to their prosperity. Let’s prosper together.